Please note: Lending options, rates, and qualifications change regularly. The information in this post is based off of requirements as of original posting date of July 2, 2024.

Achieving the milestone of obtaining a $200,000 business loan marks a major accomplishment, and our guide is ready to support you through the entire process. Choosing the right loan is vital because each financing option has its unique requirements.

As with all types of lending, you need to reach different requirements with the proper Fundability in order to fully qualify. This article is giving you the information you need to understand the starting points for some of the most common types of funding available. Additionally, it’s important to keep maximum approval amounts in mind when searching for funding. You will find each one we touch on in this article have a wide range of maximum limits. But with the correct combination, you have the possibility to reach those funding needs and wants much easier.

The table below has the requirements for each major business loan type.

The Best $200k Business Loans

| Loan Type | Requirements | Approval Difficulty |

| Bank Loan (Term Loan) | Good credit, 2 years in business, business cash flow | Hard |

| Business Line of Credit | Good credit, 2 years in business, business cash flow | Hard |

| SBA Loan | Good credit, 2 years in business, business cash flow | Hard |

| Credit Line Hybrid | Good credit | Easy (No Doc) |

| Business Credit Card | Good credit | Easy |

| Equipment Financing | Good credit | Easy |

| Merchant Cash Advance | Credit card sales, bad credit | Easy |

| Cash Flow Financing | Business cash flow, fair credit | Easy |

How to Qualify for a $200,000 Business Loan

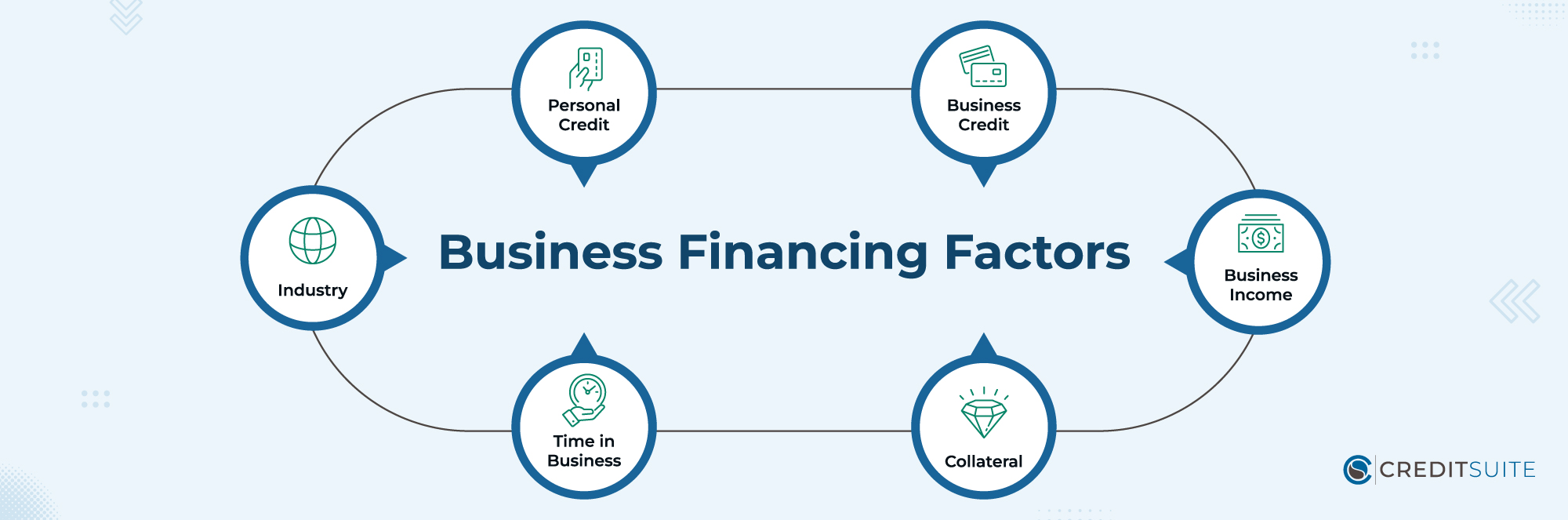

Securing endorsement for a business loan hinges on six crucial factors. Traditional bank loans require proficiency in all of these aspects, whereas alternative funding avenues might provide more leeway. These factors encompass:

- Personal Credit: Many specialized lenders catering to small businesses usually expect entrepreneurs to uphold solid personal credit ratings.

- Business Credit: Having solid business credit scores and thorough profiles can facilitate the process of qualifying for a loan.

- Business Income: Most business financing avenues usually demand some form of revenue verification as a prerequisite.

- Collateral: Obtaining approval for loans backed by assets, such as car loans, mortgages on business properties, and equipment financing, typically involves smoother processes.

- Time in Business: Several commercial lenders typically show a preference for businesses with a history extending over two to three years.

- Industry: Even with their solid financial footing, certain sectors might encounter obstacles when seeking approval.

The Best $200k Business Loan Types

Bank Loans (Term Loans)

Business loans from conventional banks are commonly labeled as term financing. This entails making consistent payments over a set “term,” usually lasting 3 to 5 years. Such loans typically come with stable interest rates.

Requirements: To meet the criteria for bank term loans, entrepreneurs typically require a strong personal credit background (FICO Scores exceeding 680), a business in operation for a minimum of two years, and yearly revenues totaling at least $100,000.

Business Line of Credit

Securing approval for business lines of credit, much like term loans, is a service often rendered by traditional banking establishments. Despite their appealing interest rates, meeting the eligibility requirements can be quite rigorous.

Upon receiving approval, you gain access to a loan that operates akin to a credit card, allowing for repeated usage. A credit limit, for instance, $200,000, is allocated, and you’re required to make incremental payments to clear the debt.

Requirements: For small business proprietors to qualify for business lines of credit, they generally require a robust personal credit background (FICO Scores exceeding 680), a minimum of two years in operation, and yearly revenues surpassing $100,000.

SBA Loans

Merging conventional banking assistance with governmental backing, SBA Loans provide advantageous terms and reduced interest rates. However, navigating the approval process for these loans can pose challenges.

Several categories of SBA loans are available, with the 7a and 504 loans emerging as favored options.

Requirements: Eligibility for SBA financing can vary, but generally, it’s expected that businesses have been operational for a minimum of one year, possess strong personal credit ratings, and demonstrate a specific amount of business revenue.

Credit Line Hybrid

Credit Suite presents a unique option called the Credit Line Hybrid, ensuring fast approval for business financing between $10,000 and $150,000, minus the need for comprehensive paperwork.

Requirements: For the Credit Line Hybrid, a good personal credit score (FICO 680+) is needed. Startups without history, collateral, or strong cash flow can also apply, easing the process.

Business Credit Cards

Business credit cards introduce an additional route for financial aid, with easy-to-meet eligibility conditions. Functioning much like personal credit cards, they grant access to a credit line which is to be repaid each month.

The main distinction between business and individual credit cards is that business ones often come with larger credit limits.

Moreover, developing a business credit profile allows entrepreneurs to secure these cards without having to rely exclusively on their personal credit histories.

Requirements: Typically, business credit cards require a solid personal credit record, and occasionally, they may also evaluate the company’s earnings.

Equipment Financing

Obtaining equipment financing offers a simpler route for qualifying compared to alternative methods.

This entails setting up either a loan or lease with regular monthly installments to acquire machinery or heavy equipment. Should you require financing, especially a loan of $200,000 for the purchase of equipment, this avenue deserves a close examination.

Requirements: For equipment financing, it’s crucial to have a robust personal credit background and an eagerness to engage fully in the procedure.

Merchant Cash Advance

Merchant cash advances operate through a business’s “merchant processing” system, managing credit card sales. In this arrangement, the credit standing of the business owner and additional elements have a lesser impact.

Once the funds are received, repayment happens automatically by taking a portion of sales, removing the need for fixed payment plans.

Given their higher financing expenses, these advances ought to be considered a last resort when other financing options are available to the entrepreneur.

Requirements: A steady monthly revenue from credit card sales, preferably more than $10,000, is highly sought after. In this scenario, less than perfect credit is considered acceptable.

Cash Flow Financing

Understanding the constraints associated with merchant cash advances, Credit Suite introduces an advantageous alternative named Cash Flow Financing. Much like merchant cash advances, the main criterion for this type of financing is the business’s cash flow.

However, Cash Flow Financing diverges from merchant cash advances by not restricting eligibility to companies that primarily generate revenue through credit card transactions; instead, it evaluates all sources of cash flow.

Requirements: Strong cash flow, at least $10,000 per month. Below average credit scores accepted.

Looking for another loan amount? Consider these articles: $900k Business Loan Options, $800k Business Loan Options, $700k Business Loan Options, $600k Business Loan Options, $500k Business Loan Options, $400k Business Loan Options, $300k Business Loan Options, $250k Business Loan Options, $150k Business Loan Options, and $100k Business Loan Options.