Please note: Lending options, rates, and qualifications change regularly. The information in this post is based off of requirements as of original posting date of July 2, 2024.

Acquiring a $40,000 business loan can pose challenges, but our guide will walk you through the steps to attain it. Given that each business loan and financial product has distinct requirements, choosing the right loan is vital.

As with all types of lending, you need to reach different requirements with the proper Fundability in order to fully qualify. This article is giving you the information you need to understand the starting points for some of the most common types of funding available. Additionally, it’s important to keep maximum approval amounts in mind when searching for funding. You will find each one we touch on in this article have a wide range of maximum limits. But with the correct combination, you have the possibility to reach those funding needs and wants much easier.

The table below has the requirements for each major business loan type.

The Best $40k Business Loans

| Loan Type | Requirements | Approval Difficulty |

| Bank Loan (Term Loan) | Good credit, 2 years in business, business cash flow | Hard |

| Business Line of Credit | Good credit, 2 years in business, business cash flow | Hard |

| SBA Loan | Good credit, 2 years in business, business cash flow | Hard |

| Credit Line Hybrid | Good credit | Easy (No Doc) |

| Business Credit Card | Good credit | Easy |

| Equipment Financing | Good credit | Easy |

| Merchant Cash Advance | Credit card sales, bad credit | Easy |

| Cash Flow Financing | Business cash flow, fair credit | Easy |

How to Qualify for a $40,000 Business Loan

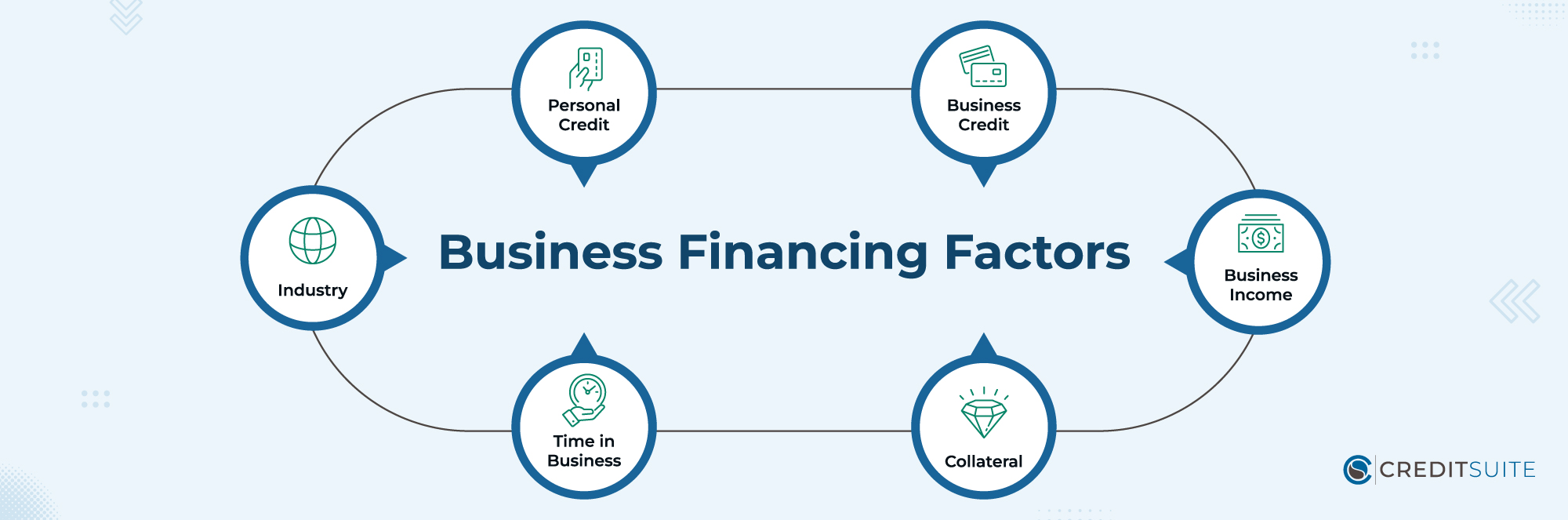

Meeting the eligibility requirements for a business loan revolves around six primary factors. To obtain traditional bank financing, adherence to all these criteria is essential. (Alternative financing avenues might offer more leeway.) These factors encompass:

- Personal Credit: A significant number of lenders specializing in small business financing anticipate that business owners will have strong personal credit scores.

- Business Credit: Established business credit scores and reports can expedite the process of obtaining loans.

- Business Income: Showing evidence of income is usually a prerequisite for most types of business financing.

- Collateral: Obtaining authorization for collateral-backed loans, such as auto loans, commercial property loans, and equipment financing, tends to be notably easier.

- Time in Business: Numerous business lenders typically require a minimum of 2 or 3 years of operational history.

- Industry: Certain sectors could face difficulties in obtaining approval, regardless of their financial situation.

The Best $40k Business Loan Types

Bank Loans (Term Loans)

Businesses often rely on traditional bank loans, known as term loans, which involve making regular payments over a set period, typically 3 to 5 years, with fixed interest rates.

Requirements:

Generally, bank term loans require a small business owner to have a robust personal credit background (FICO Scores above 680), at least two years of operational experience, and yearly earnings surpassing $100,000.

SBA Loans

SBA Loans, supported by government backing, provide advantageous conditions and reduced interest rates, similar to traditional bank loans. Nevertheless, meeting the requirements for these loans can pose a challenge.

Several types of SBA loans are available, with 7a loans and 504 loans being among the most commonly chosen options.

Requirements: Every SBA loan comes with distinct prerequisites, but generally, they require a minimum of one year in business, favorable personal credit scores, and some business revenue.

Business Line of Credit

Like term loans, business lines of credit are frequently offered by traditional financial institutions. Despite their attractive low-interest rates, meeting the qualifications for these credit lines can prove to be difficult.

When you secure a business line of credit, you obtain access to a revolving loan, much like a credit card.

You’re granted a credit limit, for instance, $40,000, from which you can repeatedly withdraw funds. Afterward, you’re obligated to make minimum payments over time to clear the outstanding balance.

Requirements: To qualify for business lines of credit, small business owners usually need a strong personal credit history (FICO Scores of 680+), a minimum of two years in operation, and annual revenue exceeding $100,000.

Credit Line Hybrid

Credit Suite provides a distinct solution known as the Credit Line Hybrid, offering funding ranging from $10,000 to $140,000, ensuring swift approval with minimal paperwork required.

Requirements: The Credit Line Hybrid requires a strong personal credit rating (FICO Score of 680+). New businesses lacking a track record, assets, or significant cash flow are encouraged to seek this option. Securing the Credit Line Hybrid is relatively uncomplicated.

Business Credit Cards

Consider business credit cards as an alternative for funding because they have simple eligibility criteria. They function much like personal credit cards, offering a credit line for immediate use and requiring gradual monthly repayments.

The key distinction between business and personal credit cards is the higher credit limits associated with business cards. Moreover, by building a business credit profile, even small business proprietors can qualify for them independently of their personal credit background.

Requirements: When applying for business credit cards, having a reliable personal credit record is usually a prerequisite. Although certain cards may also assess business income, it’s not obligatory for every card.

Equipment Financing

Considering equipment financing as an alternative can offer a smoother qualification process. It involves either securing a loan or lease with regular monthly payments to obtain significant machinery or equipment.

If you’re seeking a $40,000 business loan for equipment acquisition, exploring this option initially might be beneficial.

Requirements: Establishing equipment financing requires a robust personal credit background and a readiness to engage in the process.

Merchant Cash Advance

Utilizing a business’s credit card transactions, merchant cash advances tap into its “merchant processing” framework. Business owners’ credit scores and other elements have limited influence in this context.

Upon receiving funds, repayment occurs automatically over time, with amounts based on a percentage of sales. This eliminates the need for fixed payments.

Considering their elevated financing charges, it’s prudent for business owners to avoid merchant cash advances when other financing avenues are accessible.

Requirements: Significant monthly credit card revenue, usually amounting to at least $10,000, is highly valued. Less-than-perfect credit is acceptable in many cases.

Cash Flow Financing

Acknowledging the limitations of merchant cash advances, Credit Suite presents an upgraded alternative – Cash Flow Funding. This financing option, akin to merchant cash advances, primarily assesses a business’s cash flow for eligibility.

Unlike the restriction of financing solely to businesses with credit card sales, Cash Flow Funding evaluates all cash flow sources for qualification.

Requirements: Strong cash flow, at least $10,000 per month. Below-average credit scores accepted.

Looking for another loan amount? Consider these articles: $30k Business Loan Options, $50k Business Loan Options, $60k Business Loan Options, $70k Business Loan Options, $80k Business Loan Options, $90k Business Loan Options, and $100k Business Loan Options.