Do you have business lines of credit? Are you using them up to their fullest potential? Or are you squandering them?

Are you on the brink of taking your business to the next level but need an injection of cash? A business line of credit may be the right solution. Once approved, you’ll have access to funds that you can withdraw on an as-needed basis (up to your credit limit). Of course, you’ll eventually have to pay back everything you borrowed plus fees and interest.

So how can you best use a business credit line and avoid getting in over your head? Sometimes it helps to know what NOT to do. Here are five unwise ways to use a business lines of credit that you should definitely avoid.

#1 Cover personal expenses

This is a big one, hence, the number one ranking. If you take out a business line of credit, you may be tempted to use some of the proceeds for personal reasons. Maybe you need a little bit to make ends meet or have been waiting for an opportunity to book a getaway? That’s usually not a good idea.

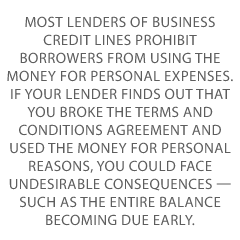

Most lenders of business credit lines prohibit borrowers from using the money for personal expenses. If your lender finds out that you broke the terms and conditions agreement and used the money for personal reasons, you could face undesirable consequences — such as the entire balance becoming due early.

Further, the purpose of the business credit line is to enable you to invest in your business so it grows, is more profitable, and is able to pay back the money you borrow. When you use the money for personal reasons, it’s not helping those causes. So when it comes to a business line of credit, be sure to keep it strictly business.

#2 Pay for routine expenses

The best use of a business line of credit is to invest it into your business so it can grow. How? Buying inventory, launching a marketing campaign, and buying equipment are all great examples.

In all of these scenarios, the money you spend should have a good chance of increasing the amount of revenue you earn. In theory, this approach can help you get off the hamster wheel of not having surplus money which causes you to need loans in the first place.

On the other hand, if you are spending borrowed money (which comes with interest charges and fees) to pay routine expenses like rent or utility bills, they are costing you more without offering returns. This can be a slippery slope you want to avoid.

#3 Borrow more than you can repay

When taking out a business credit line, it’s important to consider how much you can reasonably afford to repay. It can be tempting to take as much as you can get and hope for the best. However, a better route is to look at your historical income alongside your projections to figure out what repayment amount you can comfortably afford.

If you are expecting a revenue increase, it’s often best to base the amount you can repay on conservative ROI estimations to be sure you can afford the payments.

#4 Withdraw the funds before you need them

One of the biggest benefits of a business credit line over a loan is that you only pay interest once you withdraw money from the credit line. When you don’t need a lump sum all at once, you can save by withdrawing the funds as you need them.

For example, say that you need $10,000 to buy inventory but want to buy it in four stages that cost $2,500 each. You could potentially save by getting a credit line and withdrawing the funds as you need them versus getting the whole $10,000 upfront and paying interest from day one. However, you will have to compare the overall cost of the credit offerings available to you to see which is a better deal.

The bottom line? If you don’t need all the money upfront, don’t withdraw it until you need it!

#5 Charge unneeded business expenses

When money becomes available to you, it can get the wheels of your imagination turning. You may start thinking about office upgrades, fancy dinners out with the team, or a new tailored suit. While all of these expenses are for the business, they are not necessary to grow and don’t provide a meaningful ROI.

When the line of credit is fully withdrawn, you don’t want to be left regretful, wondering where it all went. Be sure to create a plan for how you will spend the money for strategic purposes that tie directly to growth.

Frequently asked questions about business lines of credit

Now, here are answers to frequently asked questions about business lines of credit.

What is the difference between a secured and an unsecured business line of credit?

Business lines of credit can be secured or unsecured. When secured, it means that you have to offer up some collateral in exchange for the loan. For example, you could provide assets such as inventory, equipment, or buildings. If you default when making repayments on the credit line, your lender can then seize your assets and sell them to pay off the loan.

With an unsecured business credit line, you are approved based on your credit and financial profiles. They trust that you will repay the loan. If you don’t, they can’t directly seize any of your property. However, defaulting on a loan will hurt your credit and can result in a lawsuit where they sue you to recover their losses.

Should I get a revolving line of credit?

A revolving line of credit enables you to borrow money from your credit line, pay it back, and then borrow it again (similar to a credit card). However, credit lines often have higher credit limits and lower interest rates than credit cards. If you need a larger amount of working capital on an ongoing basis, a revolving business line of credit can be a helpful solution.

Explore other small business loan options.

Borrow for your business with confidence!

If a business credit line sounds like the right move for your business, the next step is to get approved. What are the common business line of credit requirements? In most cases, you will need at least six months to a year in business and $25,000 in annual revenue. Additionally, you’ll likely need to have a “fair” personal credit score of 580 or higher.

Some lenders will want to check your business credit, and if you don’t have any history, will require a higher personal credit score. Keep in mind that requirements and terms can vary from one lender to the next so it’s smart to shop around and compare offers!